31st January 2018

WHAT’S YOUR FINANCIAL PLAN FOR 2018?

If you haven’t given much thought to your New Year resolutions, there’s still time even now and here’s one you should seriously consider. Make 2018 the year you plan your long-term wealth and get the right advice to help you achieve your goals.

Review you financial objectives

It helps to start with a clear idea of what your goals are – have they changed? Think through what your key saving, spending and investment plans are for the next 12 months and decide what you want your money to do for you. For instance, are you looking to become debt-free, save for your children, or plan your retirement spending?

Pensions

This year, you’ll be a year older and a year closer to your retirement. Pensions are one of the most efficient savings vehicles for the future, offering tax-free growth and tax relief on contributions. Plus, if you join a workplace scheme (including not opting out of pension autoenrolment), then your employer will, in most cases, make contributions on your behalf, meaning you’ll effectively benefit from free money. Sitting down with us will help you get a clear picture of how much your pension is likely to be worth, and we will be able to tell you if you’re saving enough for a comfortable retirement, or if you need to put aside more to ensure you have enough to live on in your later years.

Review your savings and investments

Don’t forget to make the most of this year’s ISA allowance. For the 2017-18 tax year, it’s a generous £20,000 or £40,000 for a couple in separate ISA accounts. ISAs are a great way to save tax-effectively; each year, more and more people are becoming ‘ISA millionaires’.

If you’ve held a portfolio of investments for a while, it might be time to review its performance. We will be able to assess the stocks and shares you hold, and ensure the balance of your portfolio remains in line with your risk profile and asset allocation strategy. A review gives you the opportunity to consider moves like selling investments that are underperforming or taking a profit from a holding that has appreciated considerably in value over the years.

Write, or update an existing Will

Dying without a Will could leave your family in disarray and facing financial worries. It’s a simple procedure that means you can decide in advance what you want to happen to your wealth on your death. You know it makes sense.

The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

The value of pensions and the income they produce can fall as well as rise. You may get back less than you invested.

ISAs – COULD YOU MAKE IT TO A MILLION?

Who wants to be a millionaire? If you would like to join this privileged group, then there is a way you might become a millionaire that doesn’t involve winning the £1m prize offered by Premium Bonds (odds 30,000:1), or taking part successfully in a television quiz show.

Individual Savings Accounts (ISAs) are a great way to invest free of tax on the income and any capital gains arising, and over the last few years the amount you can put in each tax year has risen substantially. A growing number of people are becoming ‘ISA millionaires’ as a result of rising stock market prices and the steady increase in the annual ISA allowance.

Investing for the future

The amount of money invested in stocks and shares ISAs has overtaken the amount deposited in cash ISAs, according to new data released by HM Revenue & Customs. Stocks and shares ISAs held a total of £315 billion in the 2016–17 tax year, compared to £270 billion held in cash ISAs. The number of people subscribing to stocks and shares ISAs also increased in the 2016–17 tax year to 2,589,000, from 2,539,000 in 2015–16, reversing the trend of falling subscribers in the previous few years.

If you were able to invest your full ISA allowance in a stocks and shares ISA every year, and if the ISA limit increased by around 2% each year, your investments made an annualised return of 5% after fees, and all your dividends were reinvested, you too could join the elite band of ISA millionaires in around 22 years. Of course, we must underline that this is not guaranteed because the value of your investments can and does go down as well as up.

Every little helps

If you’re not able to put away as much as £20,000 into an ISA, then remember that even smaller sums saved regularly can add up to a tidy sum over the years. Putting £100 a month into your investment ISA for 20 years could mean that if your investments grew at 5% and your dividends were reinvested, you could be looking at a fund of around £40,000. Thanks to sizeable increases in the annual allowance over the last few years, you can now stash up to £20,000 in an ISA in 2017–18. Don’t waste the opportunity.

The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

UK RETIREES INCREASINGLY RELYING ON THE STATE PENSION

Last autumn, the Financial Conduct Authority unveiled its Financial Lives Survey1, a study that tells us much about the financial arrangements made by adults of all ages in the UK.

One of the findings was that 31% of UK adults, around 15 million people, have made no pension provision to supplement their state pension entitlement and therefore could be facing a bleak future in retirement. The report highlighted the number of people aged over 50 who are not contributing to a pension and only have a few years left to build one up before they reach their 60s.

When questioned about their lack of provision, 32% of respondents said they feared they had left it too late, 26% said they were unable to afford one, and 12% said they were relying on their partner’s pension to provide an income in retirement.

Confusion surrounding pensions

Despite nearing retirement, around a quarter of those in defined contribution pension schemes didn’t know how much they had in their pension pot. Worryingly, 18% of those who have accessed a defined contribution pension in the last two years weren’t able to confirm what they had done with their money, so didn’t know if they had taken an annuity or gone into income drawdown.

Everyone approaching retirement deserves the best and most comprehensive advice which looks not only at their pension requirements, but at their wider financial planning needs. This should include a review of existing investments and savings, and financial goals such as passing money on to future generations.

Help is at hand

Whatever stage of your working life you’ve reached, it’s important to take professional advice about your pension. More and more people are realising that it’s never too late to act on their retirement planning, or too early to get their pension arrangements on track. After all, retirement should be an enjoyable and fulfilling stage of life, not a time spent worrying about money.

If you’re self-employed, an employee, work part-time, run your own business or have accumulated pension pots with past employers, your adviser can offer you the right advice to help you build up your pension pot in a tax-efficient way. And when you reach retirement, taking advice can help you make the best choices for your pension savings, and help ensure that your money lasts throughout your later years.

If you’re making plans for your retirement and would like some professional advice, then please get in touch.

1FCA, Financial Lives Survey, Oct 2017

The value of pensions and the income they produce can fall as well as rise. You may get back less than you invested.

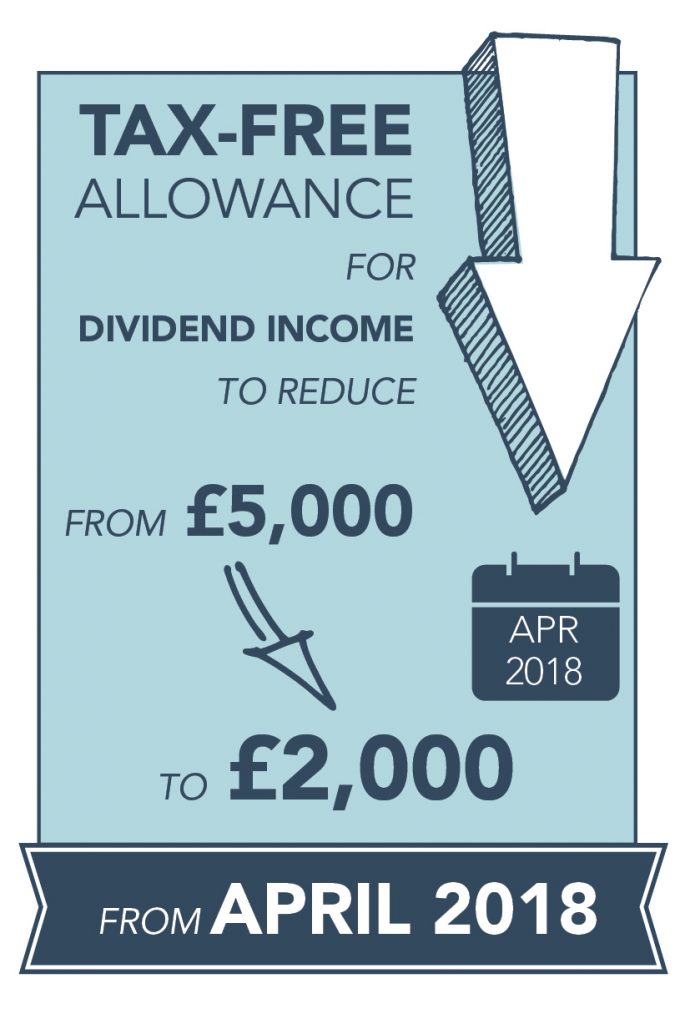

DIVIDEND ALLOWANCE REDUCTION FROM APRIL 2018

As we head towards the start of the new tax year, it’s worth remembering that the government has reintroduced its plan to reduce the tax-free allowance on dividend income from £5,000 to £2,000 from April 2018.

Many of the people affected by this measure are directors and shareholders of private companies; self-employed people often provide their services through companies, paying themselves a small salary which they top up with dividends to reduce their tax bill.

Tax shelter options for investors

This change will directly affect those with non-ISA dividend income in excess of £2,000 per annum.

In certain circumstances, investors can use existing holdings to open or top up their ISAs to shelter their investments from the taxman. This arrangement is known as a Bed & ISA. HM Revenue & Customs rules don’t generally allow investors to transfer investments they already hold directly into an ISA, but a Bed & ISA is a way of transferring assets held outside of an ISA into an ISA so that future investment income and growth are sheltered from tax. The investments are sold, cash is transferred into the ISA and the investments are repurchased. However, there will be charges, and you could end up with a Capital Gains Tax (CGT) liability if the gain you make on selling your shares together with any other taxable gains you make within the tax year exceeds the annual CGT allowance, which is £11,300 per person for the 2017-18 tax year rising to £11,700 for the 2018-19 tax year.

If you would like some investment advice on how to mitigate the impact of the cut in dividend allowance on your portfolio, then do get in touch.

The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

Tax treatment depends on individual circumstances. Tax treatment, rates and allowance are subject to change.

PROTECTION INSURANCE – HOW MUCH DO YOU NEED FOR YOUR FAMILY?

Thinking about your life insurance needs may not be the most cheerful of tasks, but arguably it’s one of the most important financial products anyone can take out, and one of the best ways of leaving loved ones provided for financially.

Life insurance provides a lump sum on death, often optionally including diagnosis of a specified critical illness, whilst wider protection cover can help provide an income for families hit by an accident or sickness.

What do you need to cover?

There is no one-size-fits-all answer to this question; the answer will depend on your personal circumstances, but there are some common scenarios. As it’s often their single biggest outgoing, many people are concerned to protect their mortgage, and provide funds to help their loved ones maintain a good standard of living if they were to die.

Parents undertake many unpaid responsibilities, including childcare, cooking and cleaning, and often want to ensure that there would be money available to provide these vital services if they were no longer around. Then there’s education – an insurance payout could ensure that children are able to continue at the same school, or can afford to go to university.

Critical illness insurance can provide a cash sum on the diagnosis of a serious illness during the policy term, and can often be combined with life insurance. Income protection insurance is a popular choice too. These policies are designed to payout if the policyholder is unable to work and earn money due to illness or injury, and, in some cases, forced unemployment.

There’s a wide range of policies and benefits available; talking to us will help you make the right choice.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK.